Credit cards have been vilified by personal finance experts like Dave Ramsey. For example, Ramsey often tells his audience on his radio show to use debit cards and get rid of their credit cards to avoid overspending. Let’s face it. When it comes to credit card use in America, consumers are racking up credit card debts that are maxing up to six figures.

On the other side of the world, like the Philippines, credit card use isn’t as prevalent in the West as banks and credit card issuers require certain income thresholds before you are approved. Out of curiosity, I joined this Facebook group that has more than 700K.

If you already have a credit card, these hacks and tips from a Facebook group called "Kaskasan Buddies" might just change the way you think about using it.

1. Qualified credit cardholders traveling to South Korea can use a simplification of visa application

South Korea won’t be just limited to our screens. You can now apply for a visa to South Korea and use your credit card statements to increase your chances of getting approved.

Image: Screenshot from Kaskasan Buddies

The embassy of Republic of Korea released its updated notice on qualified credit cards. You will still follow the standard procedure when applying for a visa. However, quoting the notice, “Bank documents are the only exempted or substituted documents” in lieu of credit card statement of accounts as proof of your income and ability to travel.

? Should you do this? This might be worth trying if you’re traveling to South Korea until next year. But don’t be filled with hope that this will be a smooth, 100% visa approval. If you read the fine print, you must go through the process and prepare the other documents to verify your identity, financial capacity, itinerary, and proof of your roundtrip tickets.

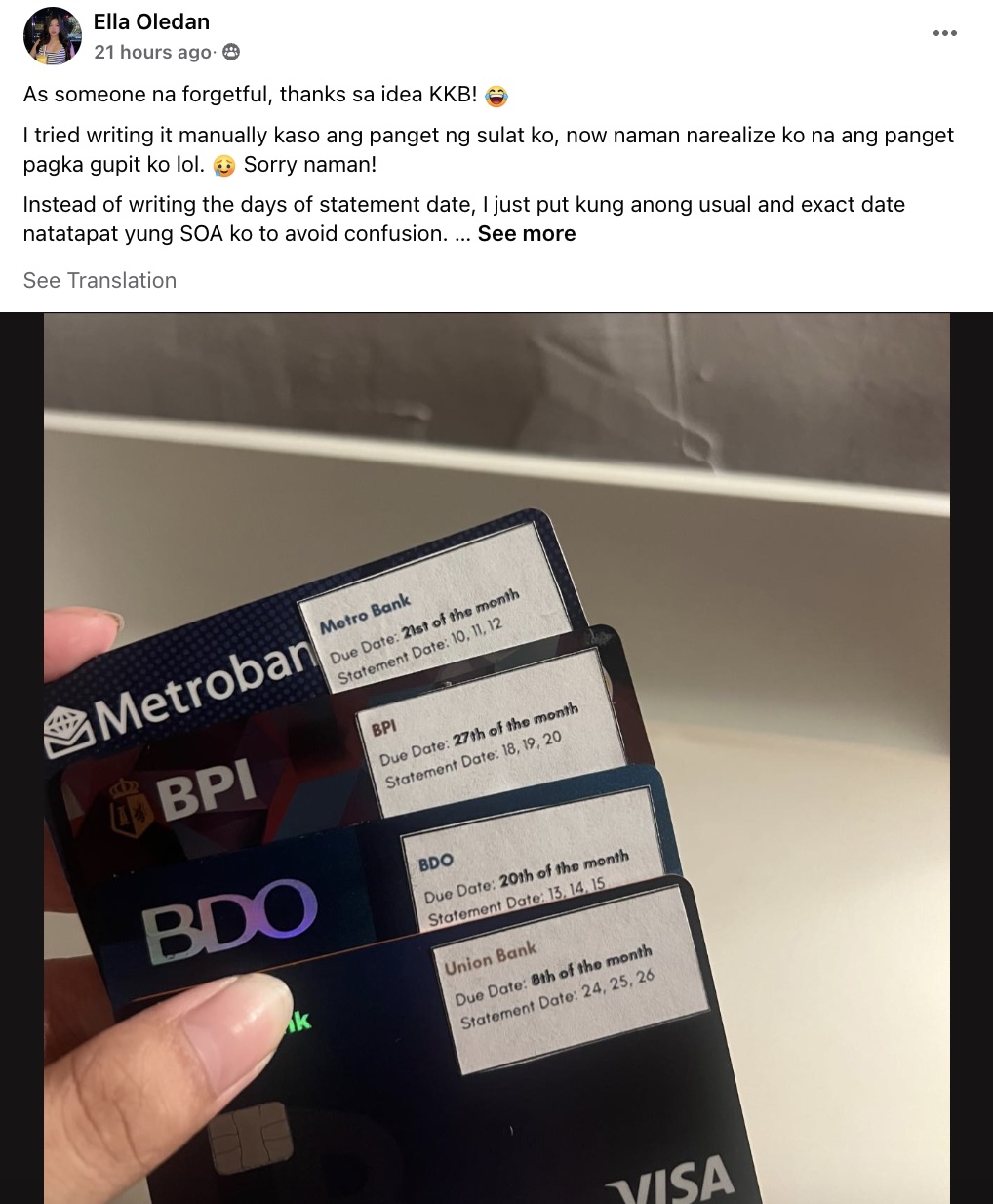

2. Solid tracking on due dates with multiple cards is possible with printed labels

What’s the best way to remember your card due date? Calendar notification? Email? For this Kaskasan ka-buddy Ella Oledan, it’s printing sticky labels on the cards. This member flexes her labels of credit cards’ due dates and statement dates. I think it’s a wise way to stay on top of the bills and make payments right on the dot.

Image: Screenshot from Kaskasan Buddies

Image: Screenshot from Kaskasan Buddies

Oledan cut out the labels and indicated the exact dates for each to avoid confusion. Some group members commended her work and told her they would do the same.

? Should you do this? This is a good practice as it provides a concrete way to track credit card dues if you have more than three cards. However, having multiple credit cards may not be sound financial advice for those who can’t control their spending.

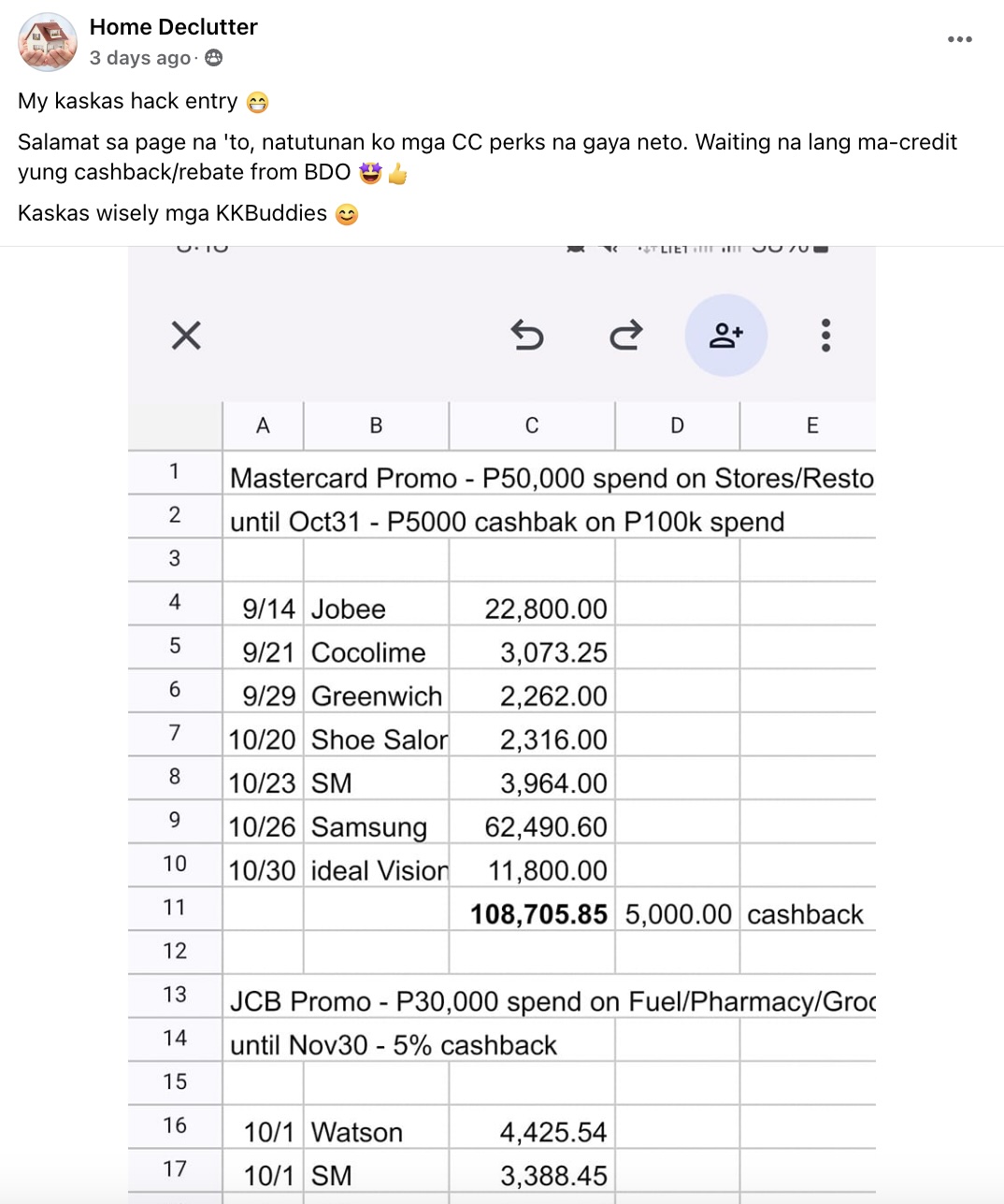

3. Effective cashback tracking with a spreadsheet file

Looking for the best way to track your cashback? One Kaskasan member, Home Declutter, still trusts the classic Excel spreadsheet. They use a spreadsheet to list every transaction, keeping tabs on total spending and monthly cashback earned. It’s a simple, reliable method to stay on top of your rewards.

Image: Screenshot from Kaskasan Buddies

Image: Screenshot from Kaskasan Buddies

You’ll notice that Home Declutter is also meticulously tracking the cashback promos to maximize the dates on when to spend before the promo ends. This is definitely worth a try, especially if your cashback credit card is armed with a high percentage of cashback rebates.

? Should you do this? Definitely, a resounding yes. This also helps you monitor your spending and when to use the credit card with a promo or cashback to redeem the rewards. A word of caution, though. While earning cashback can be motivating to track expenses and transactions, it may also lead you to overspend because you’re eager to get more rewards. Will you be spending more than ₱100,000 just to get ₱5,000 cashback in exchange for a maxed-out credit? I think that can be problematic, too, because it’s hard to maintain a low credit card utilization. Too much use of credit card limit may also send a red flag to the credit bureau because it shows you rely too much on credit.

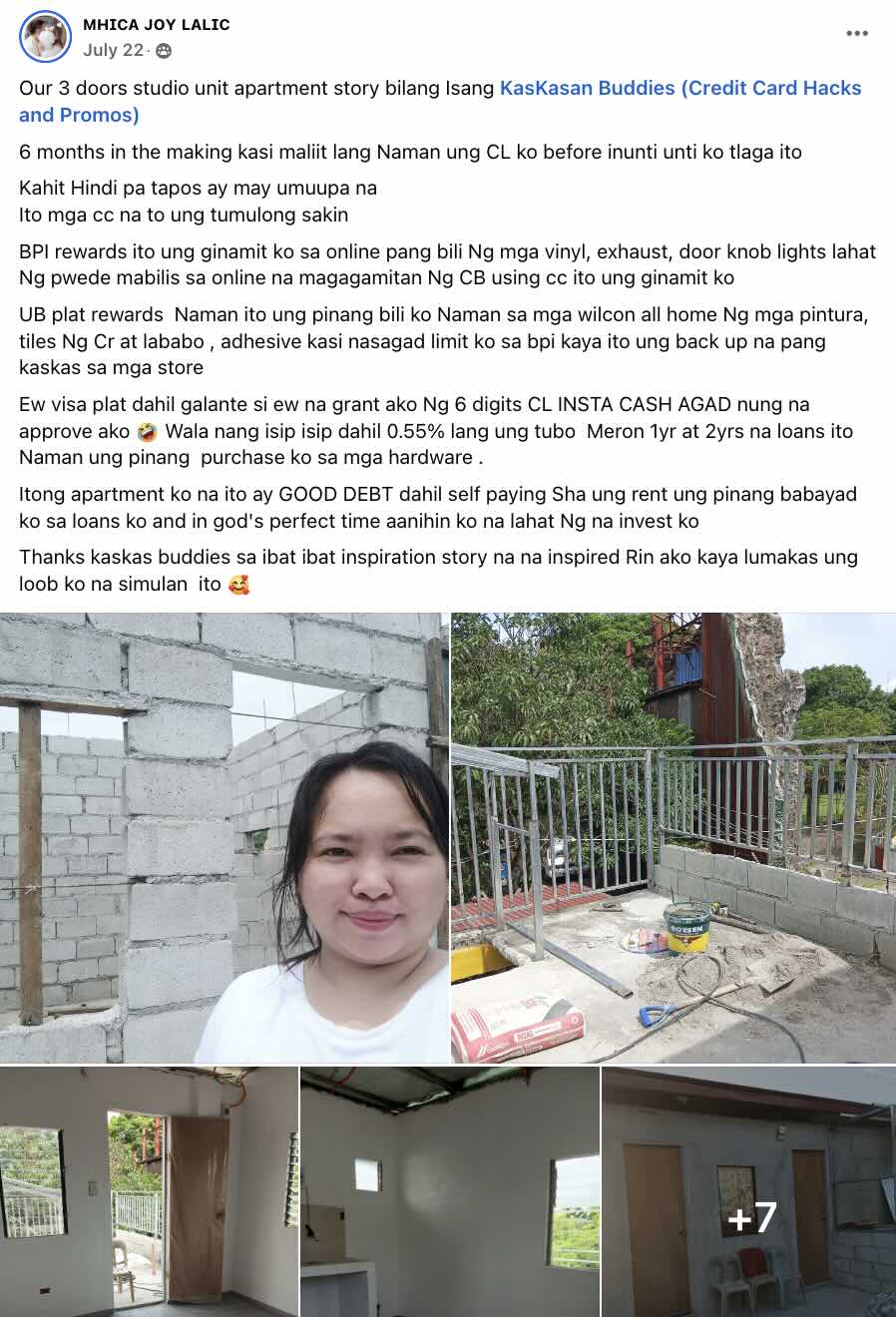

4. Invest in property improvements with credit cards and cash advances

Yes. You read that right. A member of Kaskanan Buddies flexed her rental apartment and shared how the group inspired her to use her credit cards for home improvements instead of paying cash upfront. Mhica shared that she has BPI Rewards and Union Bank Platinum Rewards credit cards and uses them to purchase hardware, electrical, and other improvements that she can buy online.

Image: Screenshot from Kaskasan Buddies

Meanwhile, her EastWest Visa Platinum credit card with a six-figure credit limit enabled her to get an instant cash loan with only 0.55% monthly interest, but she didn’t disclose the term loan. The cash was used to buy other hardware materials. This Kaskasan buddy is proud to say that she has invested in good debt because she believes the rent will be able to cover her loans and expenses.

? Should you do this? It may not be sound financial advice for all. While paying in credit for home improvement isn’t inherently wrong, not everyone is privileged to have multiple credit cards with high credit limits. Technically, the purchases fall under the category of home improvement, which can be applied as home loans and renovations with lower annual interest rates than credit card interest rates. But given that most banks have stringent loan approval in these kinds of transactions, the shiny piece of plastic card has been an alternative route for Kaskasan buddy like Mhica to build her property.

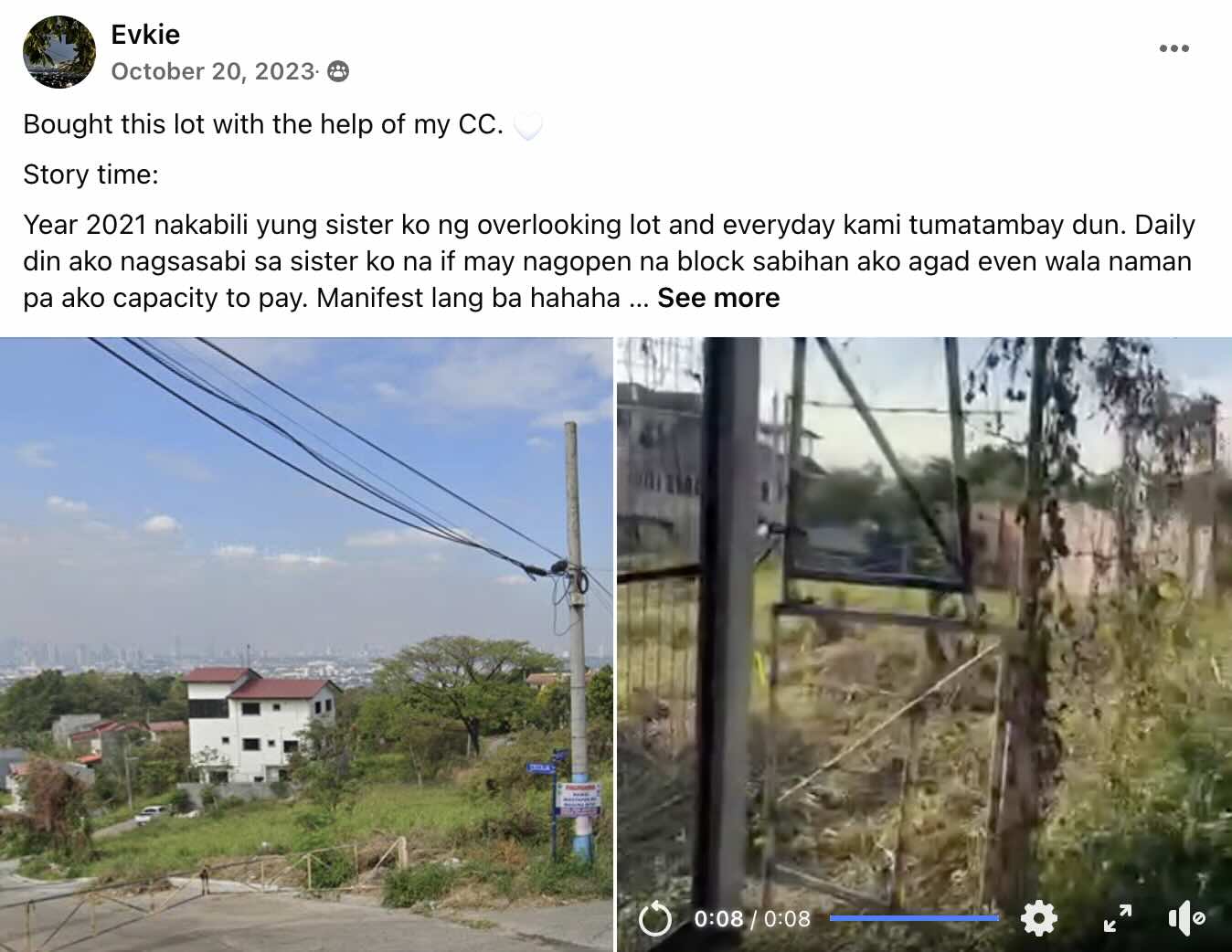

5. Buy property using your credit card limit

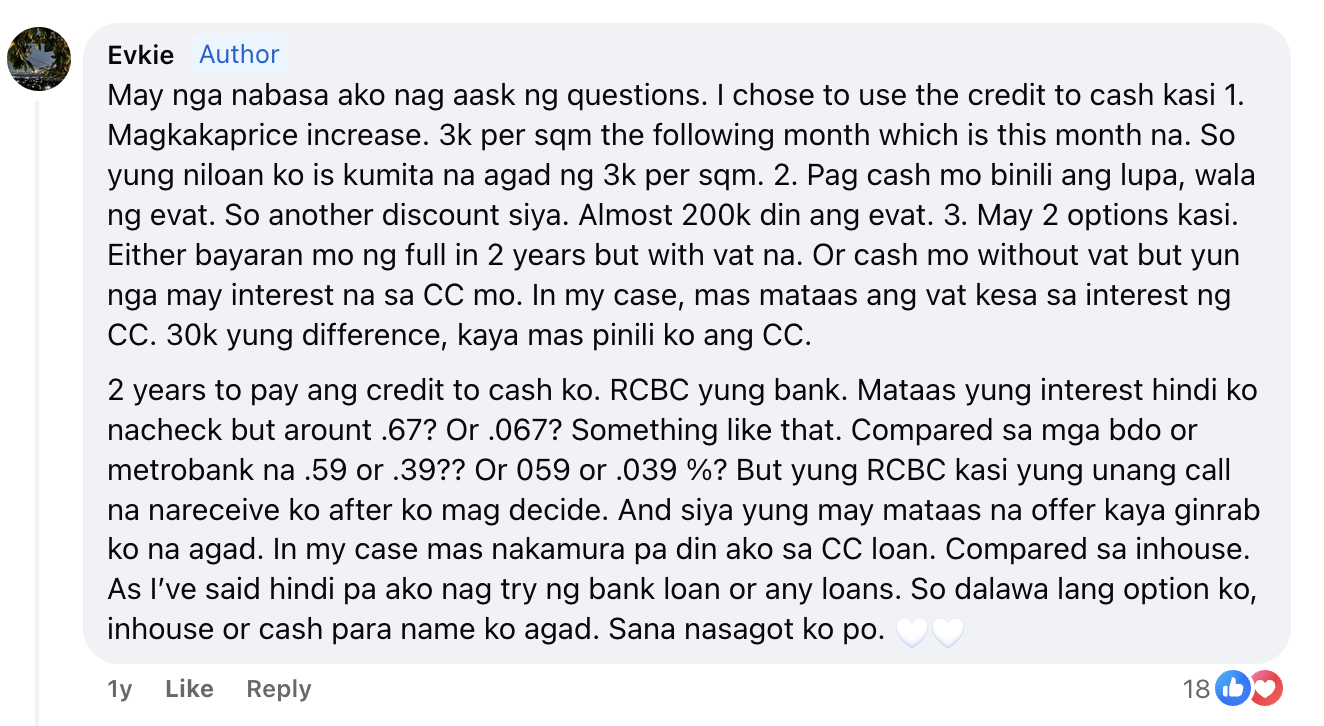

If you can use your credit card for home improvements, it’s also possible to use your credit card to buy a property. It seems too good to be true. But this Kaskasan member, Evkie, shares that he was offered by his credit card issuer, RCBC, a credit to cash worth ₱900,000.

Image: Screenshot from Kaskasan Buddies

This means that the sharer has already has a six-figure credit limit and a good credit standing—which gives the issuer a valid reason for that generous offer. Instead of resorting to a home loan, which can be a tedious process with local banks, he grabbed the opportunity and bought the property in cash.

Image: Screenshot from Kaskasan Buddies

With 283 comments, his post was a hot topic from other ka-Kaskasan buddies. Members asked about the term loan, interest rates, and other fees. He clarified that the bank offered 0.67%, payable in 2 years for the credit to cash advance.

? Should you do this? Given that the sharer has already established a good credit standing and high credit limit, it doesn’t mean that this hack applies to everyone. However, the perks of paying property in cash are that you cut the interest rates on the home loan you avail. Second, if the property, particularly a house, lot, or residential dwelling, has a selling price below 3.6 million, it is exempted from Expanded Value-Added Tax (EVAT). The sharer mentioned that because he paid in cash, EVAT is exempted—but this is not true according to research. The method of payment doesn't determine if it’s EVAT-exempt. It still depends on the nature and value of the property that was sold. It’s best to consult with a tax property consultant even before using your credit card for cash advances.

Final thoughts

The savvy credit card users in Kaskasan Buddies challenge the conventional wisdom that credit cards are financial doom. However, we must emphasize that NOT all peer-to-peer advice is sound financial advice. While we do validate and commend the achievements and results of the members who shared their financial wins, the credit card hacks are not meant to serve as the source of truth on financial advice. They also give false hopes to those who are just starting to build their credit standing.

While personal finance gurus like Dave Ramsey preach plastic abstinence, these Filipino cardholders demonstrate a more nuanced truth: credit cards can be powerful tools when wielded with discipline and strategy.

The group's creative approaches—from sticky-note due date trackers to spreadsheet cashback analytics—reveal a level of financial mindfulness that would impress even the strictest money mentor. I learned that the members are leveraging these cards for visa applications, property investments, and home improvements—all while meticulously tracking every peso of reward.

But perhaps the most valuable lesson from Kaskasan Buddies isn't about credit cards at all. It's about the power of community knowledge-sharing. In an age where financial advice often comes from polished personal finance influencers or stern experts, these everyday cardholders prove that practical money tips sometimes come from peers who've walked the path before you.

Remember: what works in one financial journey may not work in another. The key is learning from others while staying true to your financial goals and risk tolerance.