If you're looking for a traditional and reliable way of growing your money in the bank, you can place your funds in a fixed deposit account, also known as a time deposit.

Time deposits offer higher interest rates compared to a regular savings account. The bigger your deposit and the longer you keep your money in the bank, the higher your returns will be, though in the current Philippine rate environment, yields closely track the BSP policy rate, so it pays to compare before locking in.

Whether you're a casual investor hunting for the best available interest rates or simply want to start a long-term savings goal, here are the peso time deposit options from leading universal and commercial banks in the Philippines, with minimum placements and terms verified as of April 2026.

All interest rates cited below are indicative and subject to change, always confirm the latest figures directly with each bank before making a placement.

Quick comparison: Peso time deposits (April 2026)

Bank | Minimum Initial Deposit | Terms of Placement |

|---|---|---|

₱1,000 | 30, 60, 90, 180, 360 days | |

₱1,000 | 30 to 360 days | |

₱5,000 | 30 days to 1 year | |

₱5,000 | 90 days minimum | |

₱10,000 | 1 to 12 months | |

₱10,000 | 30 days to 3 years | |

₱10,000 | 30 days to 5 years | |

₱10,000 | 30 to 360 days | |

₱50,000 | 35, 63, 91, 182, 365 days | |

₱50,000 | 30 to 360 days | |

₱100,000 | 30 days to 7 years |

All interest rates cited below are indicative and subject to change. Always confirm the latest figures directly with each bank before making a placement.

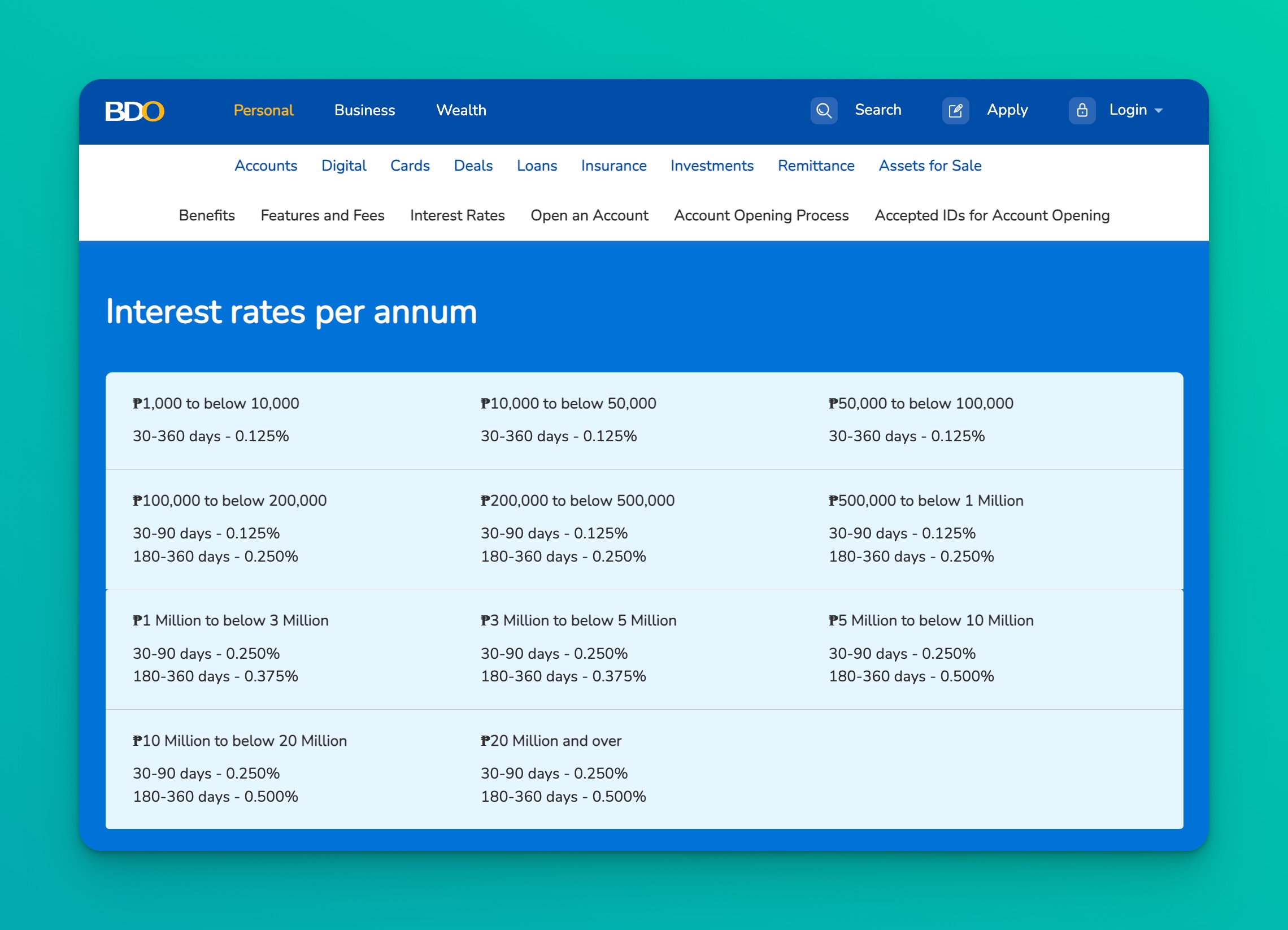

BDO Peso Time Deposit

You can make a short-term peso placement with BDO starting at just ₱1,000, with tenors of 30, 60, 90, 180, or 360 days.

As per the BDO Peso Time Deposit page, indicative rates are tier-based, ranging from 0.125% p.a. at the smallest tiers up to 0.500% p.a. for placements of ₱5 million and above on 180–360-day terms.

A 20% withholding tax applies to interest earned, and pretermination penalties apply if you withdraw before maturity.

You'll receive a Certificate of Peso Time Deposit as proof of ownership.

Landbank Regular Time Deposit

Landbank's Regular Time Deposit is accessible to most Filipinos with a minimum initial deposit of ₱1,000 and flexible terms of 30 to 360 days.

As a government-owned universal bank, Landbank is a common choice for conservative savers, OFW families, and cooperative accounts.

Visit the Landbank website or any branch for the latest indicative rates.

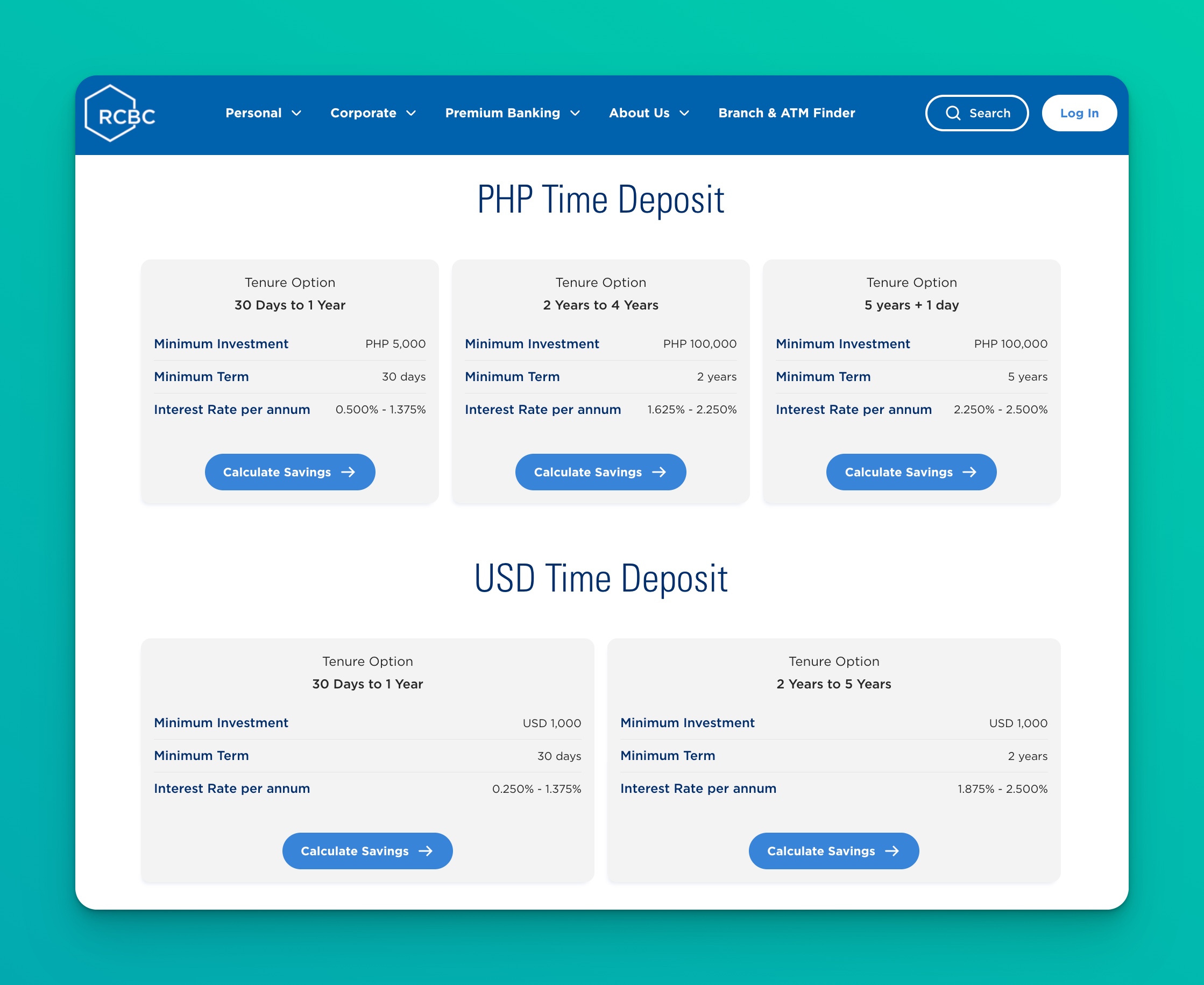

RCBC Peso Time Deposit

RCBC's PHP Time Deposit is structured in three tiers:

- 30 days to 1 year — minimum investment of ₱5,000; indicative rates of 0.500%–1.375% p.a.

- 2 to 4 years — minimum investment of ₱100,000; indicative rates of 1.625%–2.250% p.a.

- 5 years + 1 day — minimum investment of ₱100,000; indicative rates of 2.250%–2.500% p.a.

RCBC also runs a Peso Green Time Deposit starting at ₱5,000, with headline rates of 0.750%–1.500% p.a. for 30 days to 1 year, proceeds support RCBC's sustainability-linked lending portfolio.

Foreign-currency time deposits in USD, CAD, AUD, GBP, CHF, EUR, and JPY are also available at selected RCBC branches.

From time to time, RCBC runs promotional time deposit offers through the RCBC Pulz mobile app — check the app for the latest.

Chinabank Regular Time Deposit

Chinabank's Regular Time Deposit requires a minimum placement of ₱5,000 and a minimum tenor of 90 days.

Interest rates are tier-based and confirmed at your branch of account; all placements are subject to 20% withholding tax and Documentary Stamps Tax (₱1.50 for every ₱200, multiplied by the term, divided by 365 days).

Chinabank also offers Foreign Currency Time Deposits starting at USD 1,000, EUR 1,500, or CNY 5,000.

Metrobank Online Time Deposit

Metrobank's Online Time Deposit is among the more competitive offerings from traditional banks in 2026. The minimum placement is ₱10,000 and you can choose a term from 1 to 12 months, all bookable in-app.

The product is marketed with gross interest rates of up to 4.5% p.a. for eligible placements — tier-by-tier rates are published on Metrobank's time deposit rates and fees page and updated regularly.

If you need to withdraw early, Metrobank pays 25% of interest earned if the withdrawal happens in the first half of the term, and 50% in the second half. Foreign-currency time deposits are also offered.

PSBank Peso Time Deposit

For an initial placement of ₱10,000, PSBank lets you lock in at 30, 60, or 90-day terms, with optional automatic rollover on maturity. You'll receive SMS reminders as placements near maturity, and you can manage the account via PSBank Mobile and PSBank Online.

PSBank also offers a 5-Year Time Deposit for a minimum placement of ₱50,000. Placements held for 5 years and 1 day or longer are generally exempt from withholding tax, boosting your after-tax yield. For the latest indicative rates, check the PSBank website.

EastWest Peso Time Deposit

EastWest offers flexible terms from 30 days to 5 years with a minimum placement of ₱10,000.

Interest rates are tier-based and change frequently with the broader rate environment.

For current indicative rates, visit the EastWest Bank website or contact any EastWest branch.

PNB Regular Time Deposit

PNB's Regular Time Deposit starts at ₱10,000 with terms of 30 to 360 days, ideal for savers who want a mid-sized traditional bank option. Rates are tier-based and available on the PNB website or at any branch.

BPI Time Deposits

BPI offers three peso time deposit products matched to different horizons:

BPI Time Deposits

BPI offers three peso time deposit products matched to different horizons:

- BPI Auto Renew Time Deposit: ₱50,000 minimum placement, with terms of 35, 63, 91, 182, or 365 days and automatic rollover on maturity. Indicative rates range from 0.2500% to 0.7500% p.a. depending on placement size and tenor.

- BPI Plan Ahead Time Deposit — ₱50,000 minimum, 5-year term, designed for long-horizon savers with built-in tax efficiency for placements held 5 years and 1 day or longer.

- BPI Green Saver Time Deposit — ₱5,000 minimum, 5-year term, with proceeds channeled to BPI's sustainability-linked lending portfolio.

Note: BPI Family Savings Bank was merged into BPI in 2022, so there's no longer a separate BPI Family Savings time deposit product.

UnionBank Peso Time Deposit

UnionBank's Peso Time Deposit starts at ₱50,000 with terms of 30 to 360 days, and can be placed either at a branch or through the UnionBank Online app.

Rates are tier-based and confirmed at placement, check the UnionBank website for the latest indicative figures.

Security Bank Peso Time Deposit

Security Bank's Peso Time Deposit requires a minimum placement of ₱100,000, with terms ranging from 30, 60, 90, 180, or 360 days, up to 2 to 7 years. It's oriented toward higher-net-worth savers who want a mix of liquidity tiers and stronger yields. Confirm the latest indicative rates on the Security Bank deposits page.

Security Bank also periodically issues 5-Year Fixed Rate Bonds for investors seeking longer lock-in periods with quarterly coupon payments — the minimum investment there is also ₱100,000, in multiples of ₱10,000.

Other time deposit accounts available

Bank | Minimum Initial Deposit | Terms of Placement |

|---|---|---|

DBP Regular Peso Time Deposit | ₱1,000 | 30 to 360 days |

China Bank Savings Easi-Earn Time Deposit | ₱5,000 | 30, 60, 90 days |

Maybank Philippines (verify availability) | — | Maybank has restructured its Philippine retail banking; confirm current retail product availability before applying. |

For current rates and availability, visit each bank's official deposit page: DBP, China Bank Savings, and Maybank Philippines.

How do you open a time deposit account?

In 2026, most traditional banks let you open a peso time deposit either at a branch or directly through their mobile app — no need to queue in person unless you prefer the face-to-face route.

Opening in-branch

- Proceed to the New Accounts section of your preferred bank.

- Choose your time deposit product (regular, auto-renew, 5-year, green, etc.).

- Fill out the necessary forms and present your valid IDs — the PhilSys National ID is now the most widely accepted primary ID across Philippine banks.

- Fund the placement with the required minimum amount.

- You'll be issued a Certificate of Time Deposit as proof of ownership.

Opening in-app

BDO, BPI, Metrobank, UnionBank, and most other universal banks now fully support in-app time deposit placement.

You'll still need an existing peso savings or checking account with that bank as your funding source.

For a full walkthrough of what you need, see our guide on how to open a bank account in the Philippines.

Your time deposit is insured by PDIC up to ₱1 million

Effective 15 March 2025, the Philippine Deposit Insurance Corporation (PDIC) doubled its Maximum Deposit Insurance Coverage from ₱500,000 to ₱1,000,000 per depositor, per bank.

Your time deposit placements are covered by this insurance alongside your regular savings and checking deposits.

You may also read our explainer on the PDIC deposit insurance scheme and what it covers.

Things to remember before you lock in

Make sure you know what you're getting into once you put your cash in a time deposit.

- Interest is taxed. A 20% final withholding tax applies to interest earned on peso time deposits with tenors below 5 years.

- 5-year placements can be tax-exempt. Placements held for 5 years and 1 day or longer are generally exempt from withholding tax, which can meaningfully boost your after-tax yield.

- Rates track the BSP policy rate. When the Bangko Sentral ng Pilipinas' Target Reverse Repurchase Rate moves, bank deposit rates typically follow within weeks — so timing matters.

- Pretermination penalties apply. Withdrawing before maturity usually reduces your effective interest rate significantly. Some banks (like Metrobank) pay only 25%–50% of interest earned, depending on when you withdraw.

- Confirm rates before placing. Rate tables on bank websites are indicative only. Branch-negotiated rates for large placements and promotional rates via mobile apps can differ meaningfully.

- Documentary Stamp Tax (DST) — some banks (like Chinabank) pass DST on to the depositor if the placement is preterminated. Ask before you place.

Final thoughts

A time deposit is a solid option for Filipinos who want higher interest rates than a regular savings account without taking on market risk. It's especially suitable if you have a specific goal with a known time horizon , a downpayment, tuition, a wedding fund, or a retirement bucket.

The bigger your placement and the longer you commit, the more you'll earn. And while you can still access your money in an emergency, pretermination charges will eat into your returns, so only lock in funds you genuinely won't need for the duration of the term.

If you'd rather compare time deposits against high-interest savings accounts, check out our guides on fixed deposits vs. high-interest savings accounts and savings accounts that actually earn. And if you're an expat weighing your options, our guide to the best local banks for Philippine expats also covers foreign-currency time deposits.

Which time deposit product are you most likely to get? Let us know in the comments.